Table of Contents

I used to be terrified of the word “debt.” Growing up, I was taught that owing money was a moral failing—a heavy shackle that would keep me from ever being truly free. I watched people in my life struggle under the weight of monthly payments, and I promised myself I would never be one of them. Strategic Debt Management

But as I began my journey into the world of building wealth, I realized I was looking at a sharp tool from the wrong end. Debt is like fire: use it correctly, and it cooks your food and keeps you warm; use it poorly, and it burns your house down. I had to learn the hard way that not all red ink is created equal.

The Night I Realized I Was “Drowning”

I remember sitting at my kitchen table, surrounded by three different credit card statements. The numbers weren’t massive by some standards, but the interest rates were. I was paying roughly 22% interest on a vacation I barely remembered and a set of furniture that was already starting to wobble.

That was my first true encounter with Bad Debt.

Every month, I was running on a treadmill that was moving faster than I could keep up. I was trading my future hours of labor to pay for things I had already consumed. That is the hallmark of bad debt: it drains your wealth, offers no return, and carries a cost that compounds against you.

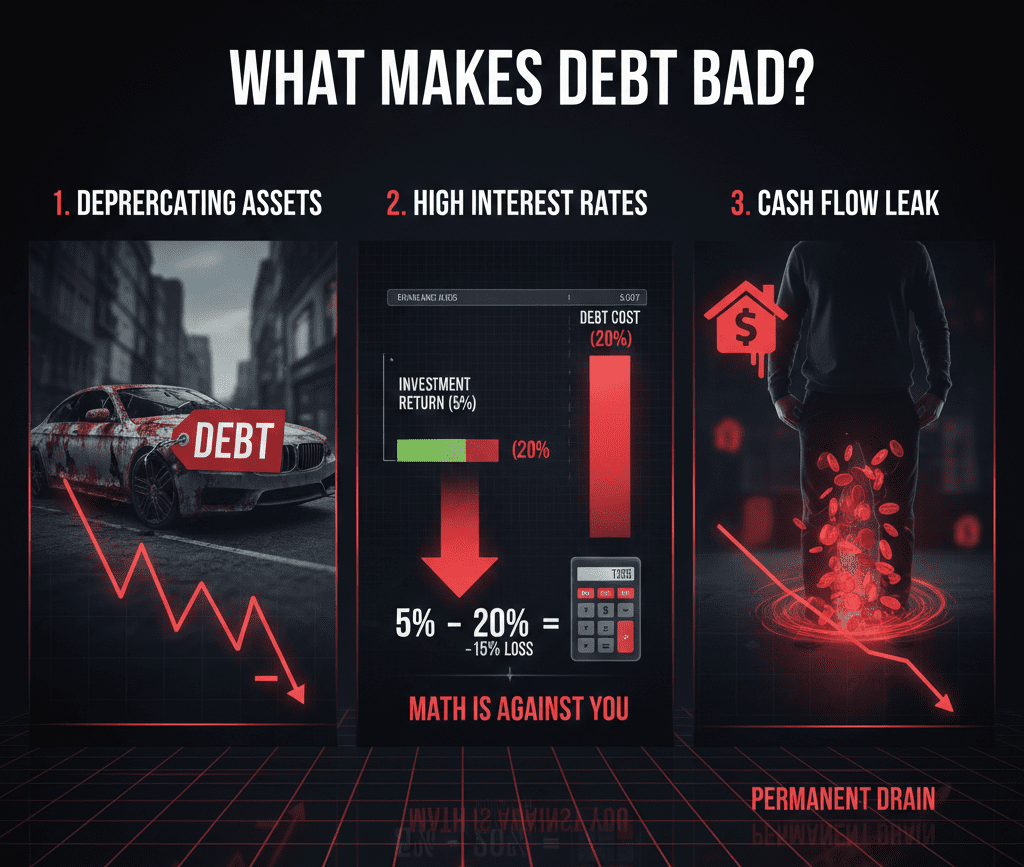

What Makes Debt “Bad”?

Through that stressful season, I developed a simple rule of thumb. Debt is bad if it meets these three criteria:

- It’s used for depreciating assets: If I borrowed money to buy it, and it’s worth less today than it was yesterday (like clothes, gadgets, or luxury items), I’m losing twice.

- The interest rate is higher than your investment returns: If my debt costs me 20% but the stock market only returns 10%, I am mathematically moving backward.

- It creates a permanent “leak” in your cash flow: It takes money out of my pocket every month without any plan to put it back.

The Turning Point: Learning to Use “Leverage”

A few years later, after I had scraped my way out of that credit card hole, I was presented with an opportunity to buy a small rental property. I didn’t have the full purchase price in cash and I was terrified. “I just got out of debt,” I told a mentor. “Why would I go back in for six figures?”

He looked at me and said, “Because this debt is an employee. It’s going to work for you.”

That was my introduction to Good Debt, also known as Leverage. I took out a mortgage—a loan at a significantly lower interest rate than my old credit cards.

Here was the difference: The debt allowed me to control a $200,000 asset with only a fraction of that in my own cash. Every month, a tenant paid me rent. That rent covered the mortgage, the taxes, and the insurance, and still left a little bit over. More importantly, as the property value increased over time, I gained the profit on the entire value, even though I had only put down 20%.

The Anatomy of “Good Debt”

I started to see a pattern. Good debt isn’t a burden; it’s a ladder. It usually shares these characteristics:

- Low Interest Rates: It’s often secured by an asset (like a home), making it much cheaper than consumer loans.

- It Buys Appreciating Assets: It’s used for things that grow in value, like real estate, or things that grow your income, like a business or a specific education.

- Tax Advantages: In many cases, the interest on good debt is tax-deductible, meaning the government is effectively helping you pay for your leverage.

- The “Spread”: If I can borrow money at 4% and use it to generate an 8% return, I am pocketing a 4% “spread” on money that wasn’t mine to begin with.

The Hidden Danger: The “Leverage” Trap

I’ve seen people get intoxicated by the idea of good debt. They think, “If some leverage is good, more must be better.” I almost fell into this trap when I considered over-leveraging myself to buy three more properties at once.

The danger of leverage is that it magnifies everything. It magnifies your gains on the way up, but it magnifies your losses on the way down. If the market dips and you owe more than the asset is worth, or if your income dries up and you can’t make the payments, that “good debt” can turn “bad” overnight.

To stay safe, I follow a strict personal “stress test”:

- Can I pay this if the income stops? I always keep a cash reserve that can cover six months of payments.

- Is the asset liquid? If I had to sell it in a hurry, could I?

- Is the math honest? I don’t calculate my returns based on “best-case scenarios.” I calculate them based on the “everything that can go wrong” scenario.

How I Categorize Common Debts Today

When I look at my balance sheet now, I don’t just see “Debt.” I see a spectrum. Here is how I personally rank them:

1. Credit Cards & Payday Loans (The Poison)

This is the ultimate bad debt. There is almost no scenario where 25% interest makes sense. I treat credit cards like a sharp knife: useful for protection and points, but I never, ever leave the blade open—I pay the balance in full every week.

2. High-Interest Auto Loans

Cars are a necessity, but they are depreciating assets. Borrowing heavily to buy a “status symbol” that loses 20% of its value the moment you drive it off the lot is a wealth-killer. I prefer to buy used and keep the loan as small as possible.

3. Student Loans (The “Grey” Area)

This is an investment in “Human Capital.” If the debt leads to a high-paying career, it’s a great investment. If the debt is for a degree that doesn’t increase your earning power, it becomes a long-term anchor.

4. Business Loans

This is one of the purest forms of good debt. Borrowing money to buy inventory or equipment that will generate immediate revenue is how almost every major corporation in the world was built.

5. Real Estate Mortgages

For me, this is the gold standard of leverage. It provides a roof over your head and a path to equity. It’s one of the few ways an average person can use the bank’s money to build generational wealth.

My Personal Philosophy for Success

I no longer fear debt, but I do respect it. I’ve realized that the goal isn’t necessarily to be “debt-free”—it’s to be “bad-debt-free” and “good-debt-optimized.” If you’re standing where I was years ago, looking at a pile of statements, the path forward is simple but not easy. Kill the bad debt first. Use the “Snowball Method” to pay off those high-interest cards. Once that weight is off your shoulders, you can start looking at the tools—the low-interest mortgages and business loans—that will actually help you build the life you want.

Wealth isn’t about how much money you have; it’s about how much of your money is working for you, rather than you working for your money.